HMRC Easement for PHEVs

Background New EU emissions rules which were recently implemented have increased the published CO2 figures for most plug-in hybrid electric vehicles (PHEVs). Whilst this change has a limited effect on private vehicle purchases, it does threaten higher company car tax rates for employees, as the benefit in kind (BiK) calculation is based on the CO2 […]

Read more

Updated Rules Now Published for Changes to ECOS Cars

HM Revenue and Customs (HMRC) has introduced new rules concerning the tax treatment of cars and vans supplied for private use under qualifying Employee Car Ownership Schemes (ECOS). These changes will impact businesses and employees who use ECOS arrangements. Announced in the Autumn Budget of 2024, this measure is intended to address loopholes in the […]

Read more

HMRC Delay Mandatory Payrolling of Benefits until April 2027

Summary In an announcement that many in the industry expected, HMRC have delayed the mandatory payrolling of benefits until April 2027. The government announced the additional time to prepare for the introduction of mandatory payrolling for benefits in kind (BiKs) and taxable employment expenses on the 28th of April 2025. They also published a technical note that […]

Read more

Ending of ECOS for Cars in April 2026

The UK Government has indicated that it intends to end the Employee Car Ownership Scheme (ECOS) from 6 April 2026. the government believes this scheme is neither legitimate nor fair, despite ECOS users being subject to heavy limitations. The scheme differs from traditional salary sacrifice schemes in that the car is owned by the employee, […]

Read more

Mandatory Payrolling of Benefits from April 2026

Background Much has changed since P11D forms were introduced in the early 1960s, and with voluntary payrolling of benefits being introduced in April 2016, it meant that adding the value of a benefit to an employee’s salary allowed payroll systems to charge the right amount of tax, hopefully improving the taxpayer experience. Up until recently, […]

Read more

Changes to Treatment of Double Cab Pickups after 6th April 2025

Background Until the budget in 2024, a majority of double cab pickup trucks were categorised at ‘van’, allowing the employees to take advantage of the the lower tax applicable to those vehicles. As you may be aware, that is changing… From 5th April 2025 From 6 April 2025, HMRC has changed its interpretation of the […]

Read more

A Copilot AI Story…

So, I asked my pc to “Write me a story about a person submitting P11Ds to HMRC”, and here is the result… Title: “The P11D Puzzle” Once upon a time, in the bustling city of London, there lived a meticulous accountant named Emily. She worked for a mid-sized company that provided various employee benefits, from […]

Read more

Deadline Day at P11D Organiser Support

The Plan Arrive at the office quite early, as there are bound to have been support tickets arriving overnight, so my plan is to try and deal with as many as I can before the phones start ringing at 9am. For context, call volumes go from about 10 a day to over 150 a day […]

Read more

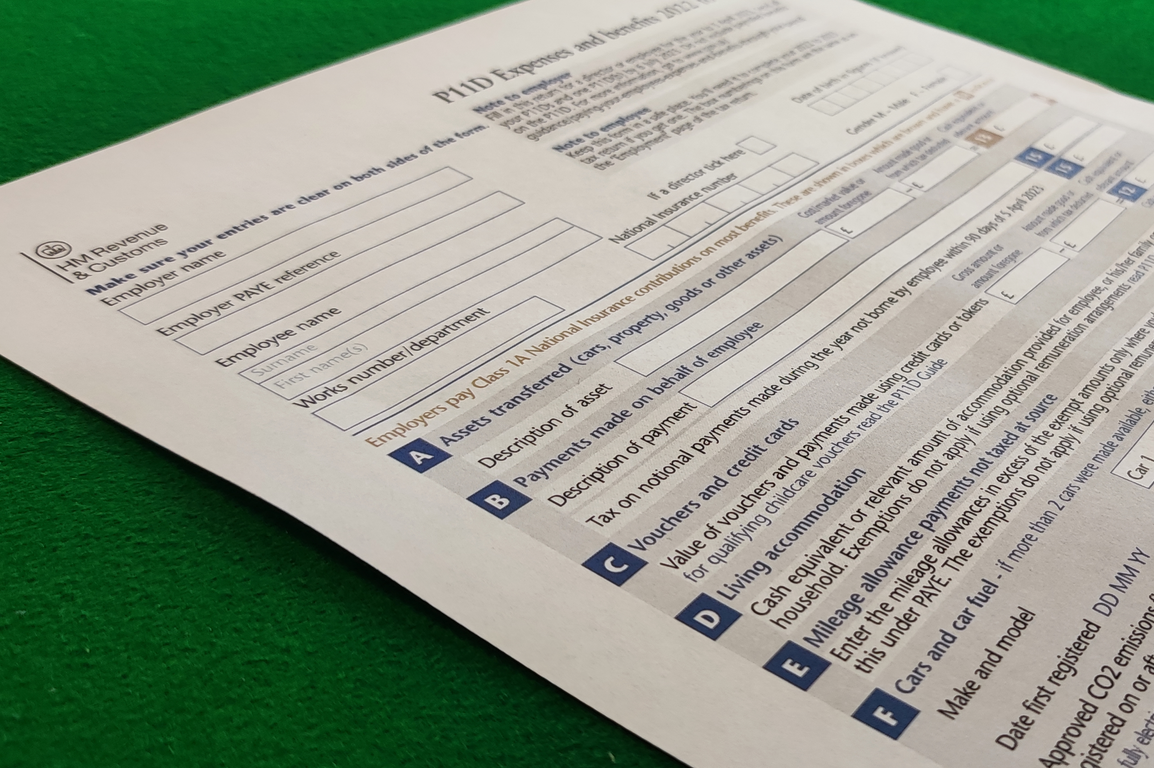

HMRC No Longer Accepting Paper P11D and P11D(b) Forms

You may have read in the latest Employer’s Bulletin that HMRC has announced that from 6th April 2023, it will no longer accept paper P11D and P11D(b) forms. An extract of the article is below: From 6 April 2023 all P11D and P11D(b) must be reported online For the 2022 to 2023 reporting year we will no […]

Read more

What’s the Difference Between AFR and AMAP?

Background When you use your car for business travel, you are entitled to claim back your ‘mileage’ so that you are not out of pocket for doing your job. The rules behind what you can claim differ based on the ownership of the car, as company cars are treated differently to privately owned cars. The […]

Read more